Don’t let Rising Interest Rates Scare You from Buying a Home, Here’s why

Are you worried about rising mortgage interest rates? You’re not alone. The days of paying 3%-4% and even 5% or 6% for a 30-year fixed-rate mortgage are long gone. One thing that is for sure about interest rates, if you are renting the interest rate is 100%.

Mortgage rates are still low compared to the rates from the last 40 years. Even if the monthly mortgage payment is now more than you originally planned just a few months ago or even a year ago, homeownership allows you to build equity and stop paying someone else’s mortgage by renting.

When buying a home it should come down to affordability in any market and any mortgage rate environment. No one should take on a mortgage payment that would put them in a non-stable financial situation. Be sure that you are ready to buy financially and comfortable with being a homeowner before taking the plunge.

“Things to Consider….”Renting vs. Buying”

With mortgage rates rising this may steer people towards renting, but keep in mind that rents have sky rocketed over the past couple of years. Nationally, rents rose a record 11.3 percent last year, according to real estate research firm CoStar Group. That fast pace of growth remained elevated in the first months of 2022, as many parts of the country continued to notch double-digit jumps in rent prices.

If you choose to rent and for example your rent is $2,000.00 a month, that’s $24,000.00 a year or $120,000.00 over 5 years! You’re basically throwing your money away while still paying a mortgage (it’s just someone else’s mortgage) and building equity for someone else.

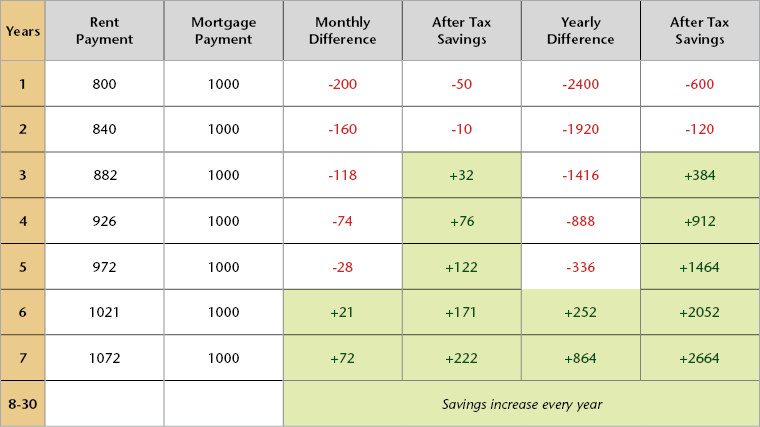

The rent payments mentioned above don’t take into consideration the year after year rent increases. Take a look at the example chart below provided by Ginnie Mae:

FACT: From 1985 to 2020, the national median rent price rose 149%, while overall median income grew just 35%, according to an analysis of publicly available data by Realestatewitch.com.

The high cost of rent means that paying a monthly mortgage is often comparable to or even cheaper than renting a home. Don’t believe it? Find out for yourself. Zillow’s Rent vs. Buy Calculator can show you how many years it will take before the cost of buying equals the cost of renting – or, the break-even horizon. https://www.zillow.com/rent-vs-buy-calculator/

Today’s higher interest rates don’t negate the benefits of owning a home. When you own a home, you gain tax advantages and you build equity over time.

When rates go up typically home prices come down, this creates more inventory which makes negotiating with sellers much easier than when it’s a sellers’ market.

“Positives of buying in this market, Yes I said Positive”

In the current Real Estate Market sellers are willing to negotiate to make deals happen. The real estate market has slowed down considerably, homes are not selling as quickly and sellers are anxious. You as a home buyer in a “buyers’ market” are in the driver’s seat, unlike the past 18+ months when buyers were over paying for homes. With that said let’s look at how you are in a great position to buy now.

If you are a first time home buyer the cost of homes are down, which means less money is needed for a down payment. For example if you were buying a $400,000.00 and were thinking of using a conventional mortgage with a 5% down payment then you would need $20,000.00 for the down payment.

- Let’s assume in this market that same house is now $350,000. , you now only need $17,500.00 down payment.

- Lower PMI or MI, The Private Mortgage Insurance or Mortgage Insurance is based on the loan amount; this means lower monthly PMI/MI payments.

- One of the factors that plays into the cost of Homeowners Insurance is the value of the home, with a lower value comes lower homeowners hazard insurance than a higher valued home.

- Inventory choices, with more homes on the market that neighborhood you love and thought you couldn’t afford may now be right in your price range.

- More inventory means more competition, this is a big advantage that could save you tens of thousands in price reductions and or seller concessions.

In a sellers market all of the above is off the table.

Things to use as a home buyer in this “Buyers’ Market “that can help you!

First and foremost you need to make sure that you are working with a Real Estate Agent that is laser focused on Real Estate, they need to know and understand the market and Must Be a Super Negotiator.

Choosing the wrong Real Estate Agent in this market especially can cost you more than the house; they can cost you thousands of dollars by negotiating the wrong deal!

I see it all the time, Real Estate Agents giving financial advice, posting things about mortgages, rates and program that they haven’t a clue what they are talking about and usually its false information or something that is so far out of line it makes no financial sense. One of my top all-time worst marketing tactic that Real Estate Agents were marketing is “marry the house, date the rate” , this is awful advice, NO ONE has a crystal ball and NO ONE should mislead buyers into thinking rates will come down to level that it would be worth refinancing later to get a lower rate. A great agent works closely with a great mortgage lender (Like me Leo Namiot) to strategize and figure out the best options for each deal they present to the sellers with your best interest first and foremost.

Be sure you are working with a competent Real Estate Agent. If you would like a referral to a great Local Real Estate Agent simply contact me, I will put you in contact with a Great Real Estate Agent that is local to your targeted purchase area.

Let’s talk about the 2/1 Rate Buy Down; I see a lot of people talking about the 2/1 buy down? So what is it and how does it work? It’s pretty basic. Let’s assume the mortgage rate is 7.00%. With a 2/1 buy down the first year/12 months of the mortgage the rate drops to 5.00%, month 13 to month 24 the rate would be 6.00% then from month 25 onward the rate goes to the actual rate of 7.00%. The seller pays for this buy down so it’s a great deal for buyers but this is something your Real Estate Agent has to negotiate on your behalf when you present your offer to purchase. This is one of the many reasons you need a great Real Estate Agent.

The purpose of the 2/1 buy down is to give the buyer a break on the mortgage payments for the first 24 months. The hope is that rates drop enough to refinance at some point within the first 24 months to make it with it or if you are planning to live in the house for only a few years.

Hold on Let’s Not Be So Quick to Jump On The 2/1 Rate Buy Down; In my 19+ years I always seek out the best options for all of my mortgage clients, with that said I have been comparing the cost to drop a

rate permanently (for the life of the loan) vs. a temporary rate buy down. I have found in many cases with my great mortgage rates that the permanent buy down is very close in cost to the sellers and provides a permanent lower rate! Don’t jump on the trends, check all your options and compare, contact me today and let’s find out what makes the most financial sense for you and your situation. Not everyone wears a size 9 shoe, what fits someone else may not fit you.

Contact Leo Namiot today, get a no obligation mortgage consultation to see if homeowner makes financial sense to you.

904-712-1500 / 203-525-3672 www.LeoLends.com NMLS#89769 Equal Housing Lender

Found this article useful? Share it with your friends

Share on facebook

Facebook

Share on twitter

Twitter

Share on linkedin

LinkedIn